Goldman Sachs India’s Manish Adukia — in a recent report — has revealed five top industry trends / strategies that can support the business growth of Bharti Airtel vs Reliance Jio.

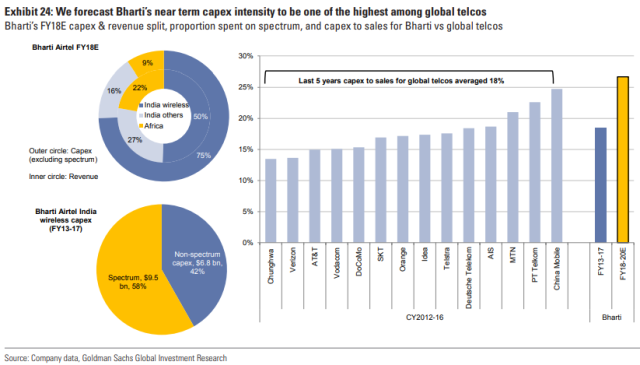

Airtel’s near term Capex (capital expenditure) intensity will be one of the highest among global telcos.

Airtel’s India wireless business is expected to be 50 percent of FY18E revenues. Airtel spent 58 percent of the Capex for buying / renewing spectrum during the past 5 years. While Airtel’s spending was for new spectrum, a significant chunk has been towards renewing existing spectrum.

Airtel’s India wireless business is expected to be 50 percent of FY18E revenues. Airtel spent 58 percent of the Capex for buying / renewing spectrum during the past 5 years. While Airtel’s spending was for new spectrum, a significant chunk has been towards renewing existing spectrum.

India’s largest telecom operator’s Capex will be focused on expanding its 4G network. Airtel does not have near term spectrum renewal (next in FY21E).

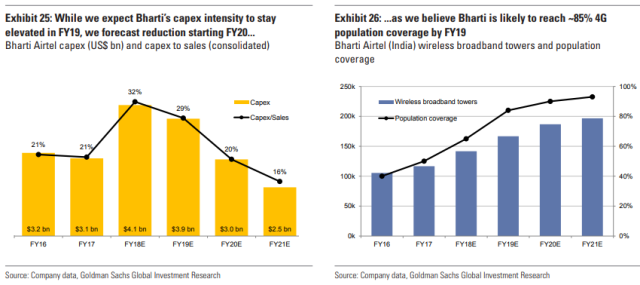

Data volume on Airtel’s mobile data network increased 6x in the past 12 months. Goldman Sachs says data on Airtel network will increase about 3x over the next 3 years. Airtel’s Capex intensity will stay elevated in FY19 and will start declining in FY20 as the company reaches >85 percent wireless broadband population coverage. Airtel’s capex to sales will fall to mid-to-high teens by FY21E.

Airtel’s strategy is to focus on other businesses which contributed 45 percent of revenues. Jio is an operator with focus on 4G data markets. Airel’s other businesses deliver robust profit growth which is not yet fully factored in by the market.

Airtel’s strategy is to focus on other businesses which contributed 45 percent of revenues. Jio is an operator with focus on 4G data markets. Airel’s other businesses deliver robust profit growth which is not yet fully factored in by the market.

Main strategies or trends

First, there will be increase in cellular tariffs in early FY19E. ARPUs will bottom out over the next couple of quarters. EBITDA for Bharti in 4QFY19 will be 26 percent higher vs that in 4QFY18E, led largely by tariff increases. The report indicates Reliance Jio will not be able to continue to offer low tariffs.

Second, Airtel has divested non-core assets in Africa, as well as stakes in its India tower and DTH business. Airtel will improve its balance sheet by selling more such assets. Airtel’s 53.51 percent stake in Infratel is worth $5 billion, about one-third its 3QFY18 net debt. Airtel may exit tower operations in the few remaining African countries. Airtel may list its Africa operations on a stock exchange.

Third, Africa business contributes about 20 percent to Airtel’s top line and EBITDA. Africa margins have headroom to expand, due to operational efficiency and topline growth. There will be 200-300 bp EBITDA margin expansion over next 3 years for Airtel Africa, reaching 38 percent by FY21E. For comparison, there will be 41 percent EBITDA margin for Vodacom, a Vodafone company in Africa, in CY20E.

Fourth, smaller telcos account for 13 percent of revenue as of Dec 2017. Aircel, which filed for bankruptcy, has 4 percent industry revenue market share and 52 million active subs. Since Aircel is largely a 2G operator, Airtel and others will benefit. Reliance Jio will not gain from the collapse of Aircel because Jio is a 4G operator.

Since about 75 percent of Aircel’s revenues comes from Tamil Nadu and category C service areas, Airtel, the market leader in these areas, could garner a large chunk of Aircel’s subs vs other telcos.

Airtel could potentially gain market share from telcos like Idea Cellular. This is because Idea Cellular is spending less on Capex in recent years. This lower Capex – one third of Airtel — will reflect in divergence in revenue growth from FY19, and Airtel will grow 400-500bp faster vs Idea Cellular.

Fifth, the proposed national telecom policy (NTP 2018), which will be implemented soon, will support the growth of Indian telecom operators including Airtel.