More than 10 markets reached fiber coverage of more than 95 percent of all homes, the 5th edition of Arthur D. Little’s Global FTTH/B Study said.

The leading fiber markets are concentrated only in a few fiber hot spots, such as Southeast Asia, the Middle East and Europe, with incumbents predominantly playing the key role in the deployments.

Open access fiber initiatives have the potential to boost fiber coverage in lagging markets, said the report. Increasing migration to a fiber infrastructure is making incumbents decide the fate of legacy copper networks.

The study shows a growing number of markets where the copper switch off has been planned (e.g. France, the Netherlands), is already underway (e.g. Sweden, Spain) or has already been finished (e.g. Singapore, Jersey).

Availability of multi-gigabit plans is limited to a handful of markets and approximately 10-15 ISPs, but in the first half of 2020 alone, we have seen at least three ISPs launch 2+ Gbps products.

Although such tariffs are still mostly a premium product, some operators (e.g. Salt in Switzerland) use them to differentiate themselves in markets that have strong incumbents and increasing competition from cable operators.

# Gigabit fiber rollout stronger than ever

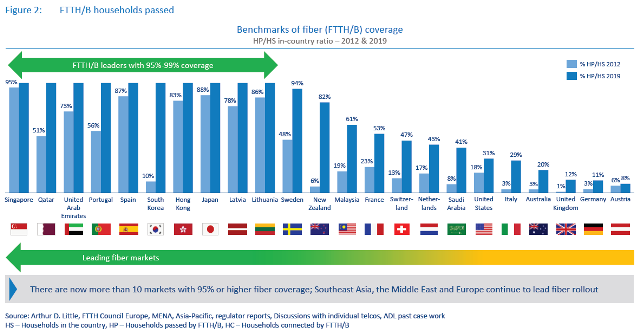

As of 2019/2020, there are more than 10 markets where fiber coverage has reached at least 95 percent of homes. In some markets, where telcos that do not have access to fiber are also actively rolling out 5G fixed wireless access (5G FWA) in order to win back market share in the gigabit broadband market.

# Fiber coverage exceeds 95 percent in at least 10 markets

Fiber deployments continue to march ahead in many markets, in line with our prediction in the previous editions of our report. Since 2012, there was an increase of 27 percent in fiber coverage among the benchmarked countries, from 39 percent in 2012 to 66 percent in 2020.

The group of countries where fiber has become almost ubiquitous – covering more than 95 percent of homes – has increased to more than 10. These markets remain predominantly only in selected geographies: Southeast Asia, Persian Gulf, and the Baltics and Iberian Peninsula in Europe.

In almost all fiber-leading markets, the incumbent has taken a principal role in rolling out fiber. However, in an increasing number of European countries, alternative operators or new open access fiber entrants have secured billions of euros to deliver promised fiber coverage in the next four to six years.

Such entities include Open Fiber in Italy, CityFibre in the UK, Swiss Open Fiber in Switzerland and Deutsche Glasfaser and inexio in Germany.

In Germany, alternative providers, Deutsche Glasfaser and inexio, which target mostly rural and underserved suburban areas, have announced plans to deploy fiber to approximately 8 million additional homes by 2030, moving the coverage from a current 11 percent up to approximately 28 percent.

Saudi Arabia is also betting on boosting its FTTH performance by launching a new open access initiative in cooperation with all operators in the market.

# Fiber take-up continues to increase with effective migration

The take-up rates of fiber services have increased in line with the improved coverage, driven by effective migration strategies. Since 2012, the average take-up rate has grown from 15 percent to 42 percent among the benchmark countries.

Singapore has achieved a fiber take-up rate of more than 95 percent after discontinuation of cable services by StarHub in September 2019 and active migration of all subscribers to the national fiber network. Fiber remains the only fixed broadband technology available to all Singaporeans.

Qatar and the UAE have also implemented effective migration programs, moving more than 85 percent of their customers to fiber.

The other driving force increasing the take-up rate is competition in the broadband market. This is particularly prominent in Portugal and Spain where fiber networks compete intensely with cable, gradually increasing the take-up rate of fiber further strengthened by the high rates of fixed-mobile convergence.

# Switch off of legacy networks picking up steam

Incumbents are announcing plans to switch off and dismantle their legacy copper networks. Singtel in Singapore turned off its copper network in 2018 and migrated its copper and cable subscribers to fiber, allowing the incumbent Singtel and cable company StarHub to switch off their copper and cable networks.

JT Global in Jersey, which already migrated its entire fixed broadband customer base to fiber, will switch off the copper infrastructure in 2020.

Operators in at least three other countries plan to completely migrate their customer base to fiber in the next four to five years

Telecoms will need to address regulatory obstacles, such as providing an alternative to existing regulatory wholesale products and replacing some copper-specific B2B use cases with other technologies.

With legacy network switch off, incumbents hope to achieve cost efficiencies especially in network operations. In recent projects, we estimate that fiber networks have up to a 15x lower fault rate and use up to 85 percent less energy compared to legacy copper-based networks.

# Fiber driving multi-gigabit offers

Telecom operators are offering 1 Gbps plans in the leading Asian fiber markets such as Singapore, Japan, South Korea and Hong Kong, opening the way for multi-gigabit tariffs.

Availability of multi-gigabit plans is still limited to a handful of markets and approximately 10-15 ISPs though the first 10 Gbps plans were initially introduced in the US, Singapore, Hong Kong and Norway more than five years ago.

Three ISPs launched Zzoomm in the UK, Orange in France and Chorus in New Zealand launched multi-gigabit offers.

However, in the majority of markets, multi-gigabit tariffs are still considered a luxury that demands a premium.

Ooredoo in Qatar charges approximately €1,600/month for its 10 Gbps plan, which results in the majority of its customers subscribing to lower-speed tiers.

Comcast’s Xfinity is the only nationwide ISP in the US with a 2 Gbps plan. At €274/month, it is three times as expensive as the 1 Gbps tariff, which is able to meet broadband needs of even highly demanding customers.

Salt Switzerland has been trying to shake up the strong position of the incumbent Swisscom in the local fiber market by launching a 10 Gbps plan in 2018. Delivered over FTTH networks of partnering utilities and bundled with a fixed line and premium TV (Apple TV), Salt’s 10 Gbps plan is offered at €46/month.

Swisscom took over two years to offer a competing product. Swisscom’s plan at €83/month is 80 percent more expensive than Salt’s. Since 2018, Salt has managed to grab more than 5 percent of the fiber subscriber base thanks to pricing strategy.

The recent partnership with Sunrise to deploy an FTTH network to over 1.5 million homes in the next five to seven years likely ensures that the market share will only continue growing.

The number of multi-gigabit markets and providers will continue increasing as a means of differentiation in the increasingly competitive broadband markets, driven by new fiber rollouts and DOCSIS 3.1 upgrades allowing cable operators to deliver 1 Gbps speeds.

Conclusion

The importance of open access fiber providers will gain, especially in important markets such as Italy, Germany, UK and Saudi Arabia, among others. Large-scale investment by non-telco entities such as energy companies and infrastructure funds will expand fiber coverage in these markets.

Gigabit tariffs have become commonplace in developed fiber markets (mostly in Asia) and are increasingly being offered to customers worldwide. However, multi-gigabit speeds are still available only in a handful of markets.

Salt in Switzerland is an example of a provider that uses its aggressively priced multigigabit offer to differentiate and disrupt the fiber market and not only as a marketing tool.