ABI Research said that CommScope has captured share in the base station antenna market, though Huawei remains the market leader.

Top vendors in base station antenna market include Huawei, CommScope, Kathrein Mobile Communication, Rosenberger, and ACE Technologies.

Together, these five vendors comprise more than 70 percent of the total market in terms of revenue.

CommScope has captured the #2 position in the base station antenna market last year as the competition in the antenna vendor market is heating up as 5G rolls out and market share is coming under serious pressure.

South Korea reported more than 90,000 5G base stations had been deployed and China had built out more than 130,000 5G base stations, ABI Research said.

Analysys Mason’s Wireless network data traffic said 5G traffic will not dominate as quickly as 4G traffic did, but it will overtake 4G traffic in 2025 (if fixed-wireless access (FWA) is included). 5G handset traffic will be similar to 4G handset traffic in 2025.

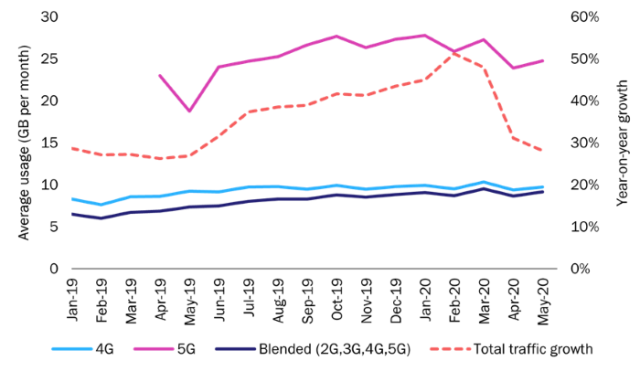

We have seen that new capacity or generations of networks and new pricing have created increasingly weak surges in traffic. This effect was seen in South Korea; the year-on-year traffic growth rate picked up after the 5G launch in April 2019, but has since fallen back to the levels seen prior to the roll-out.

“The move toward the 5G rollout is creating new challenges as the antenna and radio must be integrated for optimal utilization of site space and network performance. The successful performance of the 5G network will increasing depend on the antenna, making antenna an essential component in the operator’s network,” said Dean Tan, research analyst at ABI Research.

ABI Research forecasted growing demand for higher order number of antenna ports, such as 6 & 8 port and 10 to 16 ports. These two segments will make up more than 80 percent of the antenna shipments by 2025.

Most antenna vendors — Huawei, Kathrein, RFS — have released their versions of the Active-Passive antenna or are working with OEMs for its development. This configuration allows for an active or a Massive-Multiple Input Multiple Output (m-MIMO) antenna array to be deployed along with the passive antenna array.

The m-MIMO is key to achieving the higher capacity gains and throughput that 5G is expected to bring. However, challenges such as limited site space and difficulty of acquiring new sites, require vendors to develop innovative ideas for the 5G deployment.

Aside from the 5G focus, antenna vendors develop innovative solutions to overcome physical challenges.

Kathrein released its 378-antenna platform that generates air vortices to reduce the wind load experienced by an antenna. Wind load is a key challenge that antenna vendor wrestle with to ensure reliability and safety of the antenna and its tower.

Mobile operators in emerging and developed Markets are still upgrading and replacing their 4G antenna architecture. Almost 90 percent of antenna sales in 2019 were catering for the 4G LTE market, said Jake Saunders, vice-president for Asia Pacific at ABI Research.

Analysys Mason said 5G launches are showing characteristics of a crisis of overproduction. Operators are caught between finding or creating high-yield use cases often with more-complex value chains to justify the investment and falling back on high-volume, low-yield ones.

The opportunity for FWA may be slipping away in countries where there has been significant investment in fibre, and is almost non-existent in super-advanced telecoms economies such as China and South Korea, Analysys Mason said.